All Categories

Featured

Table of Contents

The vital difference in between common UL, Indexed UL and Variable UL hinges on how money worth build-up is calculated. In a typical UL policy, the cash worth is ensured to expand at an interest rate based on either the current market or a minimal rate of interest, whichever is greater. For instance, in a conventional Guardian UL plan, the annual passion rate will certainly never ever go lower than the current minimum rate, 2%, yet it can go higher.

In a poor year, the subaccount value can and will certainly lower. These plans let you assign all or component of your cash money value development to the efficiency of a wide protections index such as the S&P 500 Index. 7 Nevertheless, unlike VUL, your cash is not really bought the marketplace the index just offers a referral for how much rate of interest the insurance policy credit histories to your account, with a floor and a cap for the minimum and maximum prices of return.

Usually, you'll additionally have the ability to allot a part to a fixed-rate passion account. The cap is usually max credit report for a defined segment of index involvement. Most policies have annual caps, yet some policies may have month-to-month caps. Caps can change at the end of any type of sector. Furthermore, upside efficiency can be influenced by a "engagement rate" established as a percent of the index's gain.

Many Indexed UL policies have an involvement rate set at 100% (meaning you realize all gains approximately the cap), but that can transform. The 2020s have actually seen among the worst years for the S&P 500 this century along with among the very best. In 2022, the index went down 18.1%, its worst performance because 20089; the next year, 2023, the index got it all back and after that some with a total surge of 24.2%.10 We'll think you started with $10,000 in your money account on Jan.

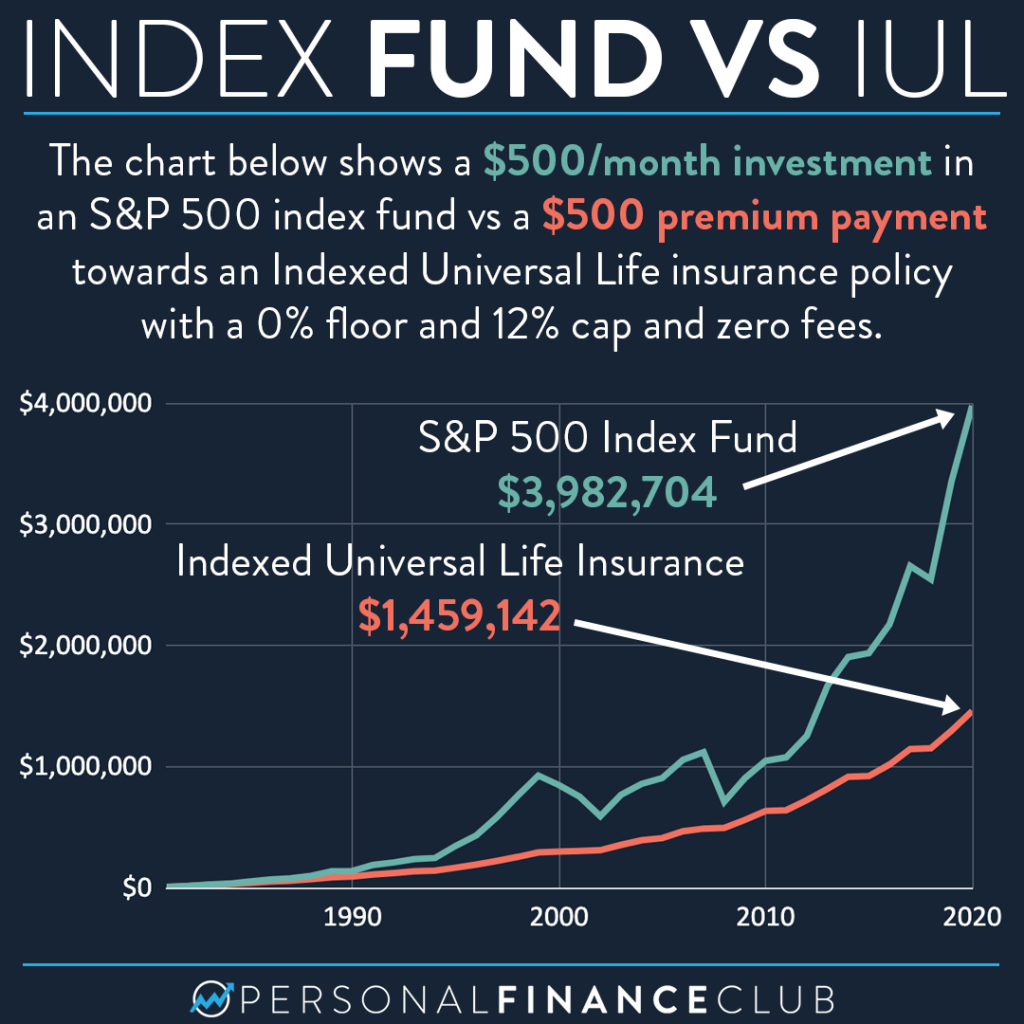

Indexed Universal Life Insurance Versus Life Insurance Policy

11 At the exact same time, you had no risk of loss in a dreadful year for the marketplace, so even 0.6% development was likely much better than other market financial investments you might have held. Assuming you made no adjustments to your appropriation, right here's what would certainly have taken place the next year: 80% S&P 500 Index$8,000 +24.2%100%11%11%$880$8,88020% Fixed-rate$2,060 NANA3%$62$2,122 Over this abnormally unstable two-year span, your typical cash value development price would certainly have been close to 5%.

Like all other types of life insurance policy, the key objective of an indexed UL policy is to provide the financial security of a survivor benefit if the insurance holder passes away all of a sudden. Having said that, indexed UL policies can be specifically eye-catching for high-income people that have actually maxed out various other retired life accounts.

What Is Equity Indexed Universal Life Insurance

There are also important tax obligation implications that insurance policy holders need to be conscious of. For one, if the policy gaps or is given up with an impressive loan, the loan quantity may end up being taxed. You should additionally learn about the "IRS 7-Pay Examination": If the collective costs paid during the first seven years exceed the quantity needed to have the plan paid up in seven level yearly settlements, the plan comes to be a Modified Endowment Agreement (or MEC).

It's important to get in touch with a financial or tax obligation professional that can assist ensure you make best use of the advantages of your IUL policy while remaining compliant with IRS regulations. Because indexed UL policies are somewhat complicated, there tend to be higher administrative fees and costs contrasted to other kinds of long-term life insurance policy such as entire life.

This advertising and marketing widget is powered by, a certified insurance manufacturer (NPN: 8781838) and a corporate associate of Bankrate. The deals and clickable web links that appear on this ad are from companies that make up Homeinsurance.com LLC in different means. The compensation obtained and other elements, such as your location, might affect what ads and web links appear, and exactly how, where, and in what order they appear.

We aim to keep our information accurate and updated, but some info may not be current. Your actual deal terms from an advertiser may be different than the offer terms on this widget. All deals may undergo extra terms and problems of the marketer.

What if we informed you there was a life insurance coverage option that combines tranquility of mind for your liked ones when you pass along with the opportunity to produce additional earnings based on certain index account efficiency? Indexed Universal Life Insurance policy, usually abbreviated as IUL or referred to as IUL insurance coverage, is a vibrant blend of life insurance coverage and a cash value component that can grow depending on the efficiency of popular market indexes. indexed whole life insurance.

IUL insurance policy is a type of permanent life insurance policy. The specifying quality of an IUL plan is its development potential, as it's connected to details index accounts.

Iul Life Insurance Meaning

Fatality benefit: A characteristic of all life insurance policy products, IUL plans additionally promise a survivor benefit for beneficiaries while insurance coverage is active. Tax-deferred development: Gains in an IUL account are tax-deferred, so there are no instant tax obligation responsibilities on accumulating profits. Finance and withdrawal alternatives: While available, any type of economic interactions with the IUL policy's money worth, like car loans or withdrawals, have to be come close to judiciously to avoid diminishing the survivor benefit or incurring tax obligations.

They're structured to guarantee the policy stays active for the insured's lifetime. Comprehending the advantages and disadvantages is critical prior to selecting an IUL insurance policy strategy. Development potential: Being market-linked, IUL policies may yield better returns than fixed-rate investments. Shield versus market slides: With the index attributes within the item, your IUL policy can remain protected versus market plunges.

became offered January 1, 2023 and offers ensured approval whole life insurance coverage of approximately $40,000 to Professionals with service-connected handicaps. Find out more regarding VALife. Minimal quantities are available in increments of $10,000. Under this plan, the elected coverage takes impact 2 years after registration as long as costs are paid during the two-year period.

Coverage can be prolonged for up to 2 years if the Servicemember is completely handicapped at splitting up. SGLI coverage is automatic for most energetic responsibility Servicemembers, Ready Get and National Guard participants scheduled to perform at the very least 12 durations of inactive training per year, members of the Commissioned Corps of the National Oceanic and Atmospheric Management and the Public Health and wellness Service, cadets and midshipmen of the United state

VMLI is available to Readily available who experts that Specially Adapted Particularly Adjusted (SAH), have title to the home, and have a mortgage on the home. All Servicemembers with full time insurance coverage need to utilize the SGLI Online Registration System (SOES) to mark beneficiaries, or lower, decline or recover SGLI coverage.

Iul Life Insurance Policy

All Servicemembers should use SOES to decline, reduce, or recover FSGLI coverage.

After the very first plan year, you might take one annual, totally free partial withdrawal of approximately 10% of the overall build-up worth without abandonment costs. If you take out greater than 10% of the build-up value, the charge applies to the quantity that surpasses 10%. If you make greater than one partial withdrawal in a plan year, the charge puts on the quantity of second and later withdrawals.

The remaining cash can be bought accounts that are tied to the performance of a stock exchange index. Your principal is guaranteed, but the amount you make goes through caps. Financial coordinators usually advise that you initial max out other retirement savings choices, such as 401(k)s and Individual retirement accounts, before considering investing via a life insurance policy policy.

{kind=link}

Table of Contents

Latest Posts

Cost Of Universal Life Insurance

Seguros Universal Insurance

New York Life Iul

More

Latest Posts

Cost Of Universal Life Insurance

Seguros Universal Insurance

New York Life Iul